| Real-Time Market Insights")

Stock Gains Without Taxes? The Secret Behind Wall Street's Top Trade

The New Trend in Wealth Management: Embracing Losses

With the stock market hitting record highs, it's no longer enough for wealthy investors to just make money. In fact, they're now focusing on losing money as well. This unusual shift is driven by the need to offset capital gains taxes, and it has led to a new investment strategy that promises both index-beating performance and tax losses.

This strategy is particularly appealing to investors who have significant gains in concentrated stockholdings. These could be shares of major tech companies like the Magnificent Seven, traditional index funds, or even employee stock options from fast-growing tech firms.

Traditional Tax-Loss Harvesting Strategies

The traditional method for managing these gains is direct indexing, a form of tax-loss harvesting that has been around since the early 2000s. According to research firm Cerulli Associates, there is currently $1.1 trillion invested in this strategy. However, as the market continues to rise, direct indexing is becoming less effective at generating the necessary losses.

According to Jon Diorio, head of U.S. wealth product at BlackRock, around half of such portfolios are now "ossified," meaning they no longer generate losses. This has prompted financial advisers to seek out more innovative strategies to help their clients manage their tax liabilities.

The Rise of Long-Short Tax-Aware Strategies

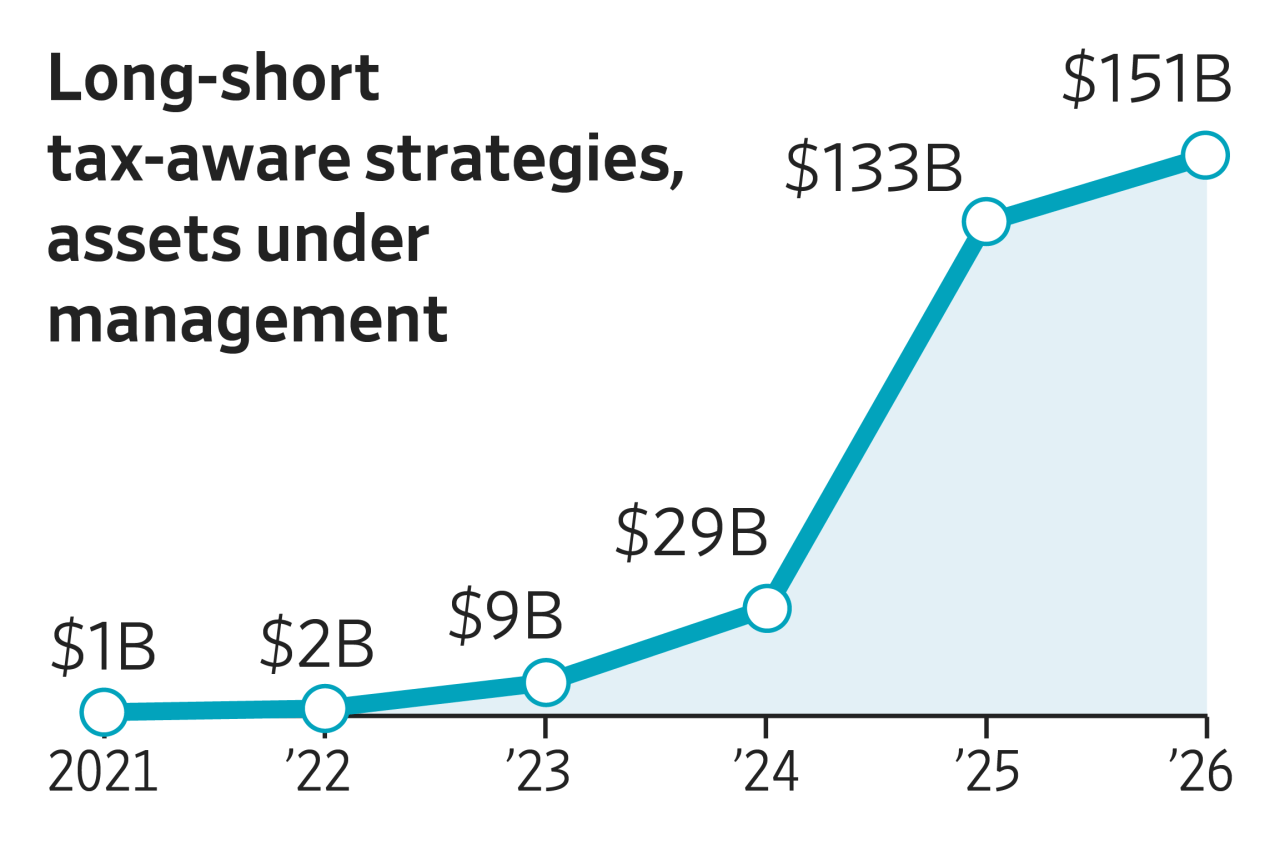

A newer approach, known as long-short tax-aware or tax-aware alpha, has gained traction among wealthy investors. This strategy involves using leverage to generate more losses, which can then be used to offset capital gains elsewhere in the portfolio. Over $150 billion has flowed into this type of tax-loss harvesting, according to Brent Sullivan, who writes about the industry on his Substack, Tax Alpha Insider.

The strategy was initially developed by hedge-fund firm AQR Capital Management for clients such as family offices and ultra-wealthy individuals. Around five years ago, the firm and its rival, Quantinno Capital Management, began allowing individual investors and their advisers to tailor the strategy within their own separately managed accounts (SMAs).

Custodians like Fidelity Investments have made this strategy more accessible by lowering investment minimums, leading to widespread adoption. AQR now manages nearly $70 billion in tax-aware long-short strategies, with roughly 80% of that in SMAs. Quantinno manages over $48 billion, and many others have followed suit.

Balancing Performance and Losses

Long-short managers aim to achieve "alpha," which means outperforming the benchmark while also harvesting losses. This balance between performance and loss generation is crucial to the success of the strategy.

However, the popularity of this approach has led some custodians, such as Fidelity and Charles Schwab, to impose limits on new accounts. Both direct indexing and long-short SMAs come with their own set of risks.

Direct-indexing managers may struggle to track the index if they cannot find suitable substitutes for the stocks they sell. Additionally, the IRS’s "wash sale" rule restricts the ability to recognize a loss on the sale of stock if the same stock is purchased within 30 days before or after the sale.

Practical Considerations for Investors

Neither strategy is likely to eliminate all capital gains in a bull market. The losses generated are typically used to offset gains in other parts of the portfolio. For example, an investor selling a stake in a business at the start of the year might invest the proceeds into a long-short SMA to generate losses that can offset some of their capital gains by the end of the year.

However, holding onto winning investments can lead to new gains building up over time. These gains will eventually be taxed when the investor cashes out.

Michael Paulus, founder of wealth manager PCM Encore, recommends direct indexing for most of his clients, especially those nearing retirement who will need to sell highly appreciated stocks to fund their retirement. Direct-indexing managers charge annual fees as low as 0.05%.

Paulus is more cautious about using long-short SMAs. He uses them for clients expecting a major one-time gain, such as from the sale of a business, or for clients in tech who receive a large portion of their pay in stock. Otherwise, he avoids them due to the higher costs associated with the strategy.

Tax-aware long-short strategies can cost as much as 1.5% to 3%, including investment management, financing, and borrowing fees. Paulus humorously remarked, "All else being equal, I’d probably rather cut the government a check than a hedge fund in Connecticut."

Investors must carefully weigh the benefits and risks of these strategies to determine what works best for their financial goals and tax situation.

{kind=link}

Post a Comment for "Stock Gains Without Taxes? The Secret Behind Wall Street's Top Trade"

Post a Comment